InsurTech companies raised over $800m-worth of funding in the second quarter of the year across 34 deals

- Q2 2017 had 17.2% more deals and over double the overall investment compared with Q2 2016. The $822m total eclipsed the levels set by the second largest quarter in the period, Q1 2016, by almost $200m, despite seeing 46% less deals.

- Q2 2017’s overall investment total for InsurTech was in stark contrast compared to the trend in the five previous quarters. Between Q1 2016 and Q1 2017 there was a continuous QoQ decrease in overall InsurTech funding, as investment fell from $630.4m to just $189.8m in Q1 2017 – a fall of nearly 70%.

- The number of deals per quarter was more volatile than the investment total. Deal activity peaked in Q1 2016 with 63 and saw its lowest point in the following quarter with 29.

- The quarter with the highest average deal size was the quarter that just closed; Q2 2017’s average funding round received by an InsurTech company was $24.2m. The top eight deals of 2017 so far all came in the second quarter of the year.

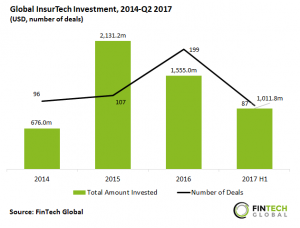

InsurTech investments had a strong start to the year with funding in the first half of 2017 is almost two thirds of 2016’s total

- 2016 was global InsurTech’s most active year to-date with 199 deals spanning the year. This was an increase of 86% compared with 2015’s total and over double 2014’s total of 96. The number of deals in the 2014-2016 three-year period rose at a CAGR of 27.5%.

- Over $2.1bn was invested across 2015 into InsurTech companies, spearheaded by Chinese firm ZhongAn’s $934m Series A. The investment came from CICC, CDH Investments, and Morgan Stanley.

- 2015’s average funding round size was $19.9m, the highest in the period. The first half of 2017’s average investment size in contrast is $11.6m. 2017 looks set to come close to surpassing both 2016’s record deals haul and 2015’s record total investment.

UK-based Gryphon received the largest InsurTech investment of Q2 2017 with $230m

- The top 10 investments received by InsurTech companies across Q2 2017 totalled over $700m – more than 90% of InsurTech’s overall funding for the quarter. The largest investment went to London-based Gryphon (aka Gryphon Group Holdings Limited). Gryphon is a new startup in the InsurTech space and has the intention to design and build an insurance challenger ‘with an ambition to protect more families in the UK’. They were one of only two European-based firms in the top 10, with Swedish company BIMA also on the list with the ninth largest deal.

- Six of the top 10 are headquartered in the US, with Bright Health leading the way for US InsurTech investment having received a $160m-valued Series B funding round at the start of June. The round was led by Greenspring Associates with co-investment coming from Greycroft Partners and Bessemer Venture Partners, among others. Minnesota-based Bright Health offers health insurance options direct to consumers both through public and private exchanges.

- Asian headquartered firms comprise the remainder of the top 10. They are made-up of India-based duo Acko General Insurance and Coverfox Insurance, as well as Singaporean firm Singapore Life, a life insurance firm founded in 2014 that offers protection solutions both digitally and through financial advisers.

Europe has emerged to become one of InsurTech’s leading regions since 2014

- Investments going to European InsurTech firms rose YoY in the 2014-2016 period. Its share of global funding continued to rise in 2017 where the region saw its share increase to a third – a percentage which would be a record for the continent if continued until the end of the year. 2017’s rise for Europe was led by the UK, who alone received 14 separate rounds of funding in the InsurTech space in the first half of 2017, nearly half of the overall deals that went to European-based firms in the period.

- North America’s proportion of global InsurTech investments fell YoY in the period 2014-2016, and has also seen a further fall in 2017. The region still leads global InsurTech funding but has seen its deal share fall over 20% since 2014 – a decrease from 68.8% to 47.1%.

- While Europe’s share of InsurTech investments has seen a steady rise since 2014, Asia-based InsurTech firms have seen the opposite. Europe and Asia had 17.8% apiece of the global InsurTech funding in 2015, whereas in 2017 so far, they are 21.8 percentage points apart.

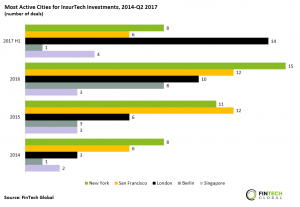

London overtakes New York and San Francisco to lead global InsurTech investment for the first half of 2017

- London-based InsurTech companies received 14 separate investments across the first half of this year. This sees the UK capital overtake US FinTech hubs New York and San Francisco to the top spot, who have led investments into the InsurTech space over the past three years.

- New York is still InsurTech most frequent place for investment overall however. InsurTech companies based in the city have received 42 separate funding rounds since the start of 2014 – more than any other city worldwide.

- Combined, the top five cities received 136 investments – 32.2% of the total InsurTech deals in the period. Berlin and Singapore round of the top five with 13 and 12 deals each in the period, respectively.